How to protect your loved ones after you die

Experts explain how passing away without a will can cause problems for your family and how to take the first steps toward making one.

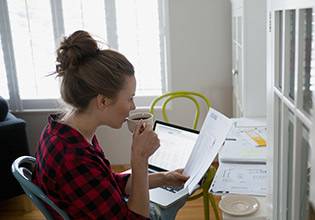

Clearer investment statements to support confident financial decisions

See how upcoming statement enhancements can give you a clearer view of your fees and help you stay confident in your long‑term plan.

Time well spent: Have you checked your beneficiaries lately?

There's few limits around whom you can name. But ensure your choices are up-to-date and align with your wishes.

Discover the difference of segregated funds

Unique insurance-based investment offers helpful estate-planning features.

It's time to spring clean your finances

You may be thinking about doing a little spring cleaning to tackle tasks that have gone undone in the hustle and bustle of life. This season is the perfect time to make sure you’re on the right track towards your goals. Here are a few ideas to help you spring into action.

Buying a house and life insurance

There’s mortgage protection insurance, life insurance and mortgage loan insurance. How are they different and how do they help you when buying a house?

8 tips to consider when searching for a new home

When it comes to investing in a new home, location is key, but there are other factors to consider to determine how much your house is worth.

How finances can impact your overall health

Your mental, physical and financial health go hand-in-hand.

7 financial mistakes to avoid in a separation or divorce

Getting divorced or going through a separation can disrupt your life and your finances. Learn how to keep your finances stable at this critical time.

Organizing your important documents

Make things easier for loved ones and the executor of your will by organizing your important legal, financial and other documents.

10 simple money management tips

From creating a comprehensive budget to how to work with an advisor

4 ways to declutter your finances

Get your finances organized – budgeting, managing debt, planning for retirement and preparing a will.

The freedom of flexibility

Manulife One offers a flexible mortgage product that adapts to you and your needs to help you achieve your life goals.

Poised, postured and prepared

Yoga studio owner and teacher at Toronto Yoga Mamas discusses the relationship between physical and mental fitness and financial health.

Clearing the clutter: 4 financial tips

Being financially organized contributes greatly to feeling financially prepared.

Finances got you frazzled?

Avoid money mistakes to keep your goals within reach.

Understanding probate and wills

An introduction to this important legal process